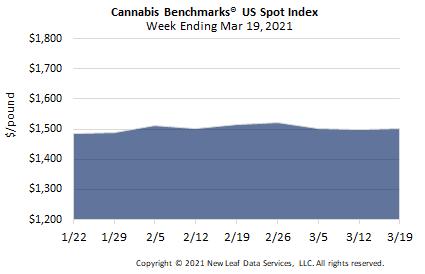

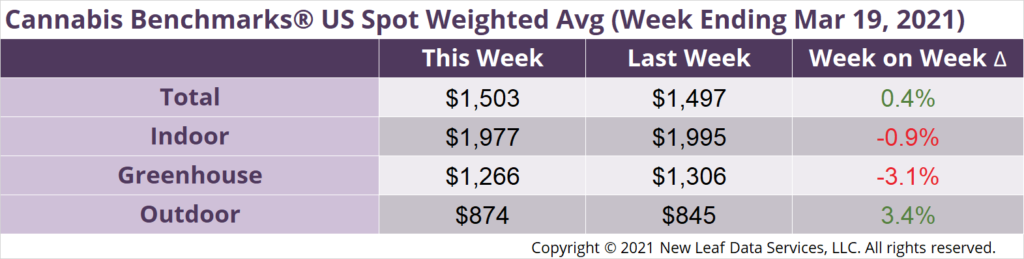

U.S. Cannabis Spot Index up 0.4% to $1,503 per pound.

The simple average (non-volume weighted) price decreased $12 to $1,757 per pound, with 68% of transactions (one standard deviation) in the $987 to $2,527 per pound range. The average reported deal size was 2.3 pounds. In grams, the Spot price was $3.31 and the simple average price was $3.87.

The relative frequency of trades for outdoor flower decreased by 2%. The relative frequencies of deals for indoor and greenhouse product increased by 1% each.

The relative volume of outdoor flower contracted by 3% this week. The relative volumes of warehouse and greenhouse product expanded by 1% and 2%, respectively.

![]()

After a turbulent 2020, marked by the disruption of previously-established trends in sales and wholesale price movements during the COVID-19 pandemic, the U.S. Spot Index and monthly revenue figures out of numerous markets have shown stability through the early months of this year. In this week’s Premium Report, we examine adult-use sales figures out of Massachusetts in the first two months of 2021, which exhibited continued growth, albeit at subsiding rates compared to the end of 2020. Wholesale activity in Alaska’s relatively small adult-use market also saw a boost in January. We noted in last week’s report that an uptick in sales in Colorado in January broke with behavior observed in prior years, suggesting the possibility of the persistence of strong demand growth documented in 2020.

Meanwhile, revenue figures from the first 10 days of adult-use sales in Arizona, released by state officials this week, are significantly lower than those seen in the early days of Illinois’ recreational system, which launched a bit over a year ago. This despite Arizona’s more robust retail and production footprint relative to those in Illinois at the outset of 2020.

Looking ahead, how supply and demand trends will play out with the end of the coronavirus crisis seemingly within sight has yet to be determined. Federal stimulus payments were distributed to millions of individuals this week, providing an increase in disposable income to some. Such disbursements last year did not coincide noticeably with changes in monthly sales figures, however, and March is typically a month that sees a surge in purchasing in both adult-use and medical markets regardless.

Increased employment as COVID-related restrictions are eased and eventually eliminated should provide a more regular source of expanded income to those whose jobs have been impacted negatively by or lost to the virus. On the other hand, though, there will also be more outlets for disposable income apart from cannabis, as businesses such as movie theaters, theme parks, and sports and entertainment venues are permitted to reopen and operate at full capacity. Additionally, a shrinking number of individuals will presumably be working from home as this year wears on, curtailing opportunities for increased cannabis consumption that presented themselves in 2020.

Finally, the cessation of the stress and anxiety generated by COVID-19 and its attendant effects on society could conceivably have divergent impacts on the robust demand for cannabis observed last year. Many have attributed 2020’s record-breaking cannabis sales in part to consumers attempting to self-medicate with cannabis products to mitigate the negative psychological impacts caused by the coronavirus. Without that impetus, consumption may stabilize or even decline, although there is also the possibility that use habits developed in 2020 could persist even as day-to-day life returns to “normal.”

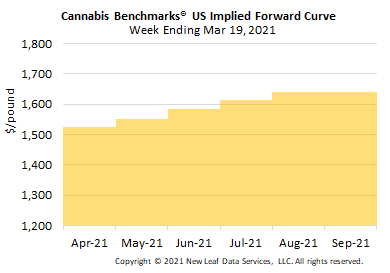

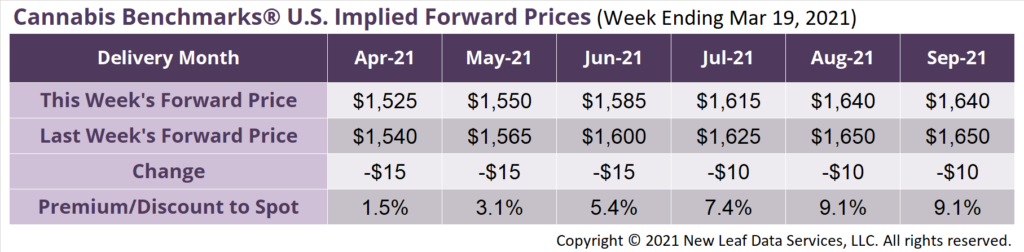

April Implied Forward down $15 to $1,525 per pound.

The average reported forward deal size was unchanged at 47 pounds. The proportions of forward deals for outdoor, greenhouse, and indoor-grown flower were 58%, 32%, and 10% of forward arrangements, respectively. The average forward deal sizes for monthly delivery for outdoor, greenhouse, and indoor-grown flower were 59 pounds, 32 pounds, and 25 pounds, respectively.

At $1,525 per pound, the April Implied Forward represents a premium of 1.5% relative to the current U.S. Spot Price of $1,503 per pound. The premium or discount for each Forward price, relative to the U.S. Spot Index, is illustrated in the table below.

Colorado

Vertically Integrated Adult-Use Cultivators Will See 24% Decrease in Tax on Internal Transfers of Flower in Q2

Arizona

Recreational Sales Reached $2.9 Million in Final 10 Days of January, a Slower Start Than Some Other States

Massachusetts

State Data Shows Adult-Use Demand Continued to Expand in January and February, But Rate of Growth Slowed

Oklahoma

Bill Approved by State House of Representatives Would Set Cap on Licenses