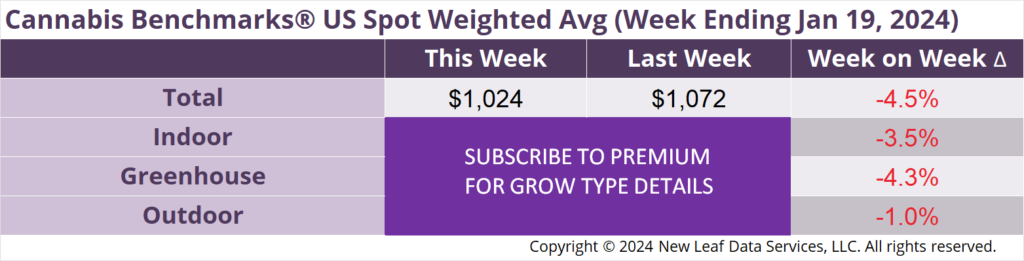

The U.S. Cannabis Spot Index decreased 4.5% to $1,024 per pound.

In grams, the Spot price was $2.26.

After price action in December and early January gave the impression that a pronounced downtrend might not be in the offing, the U.S. Spot Index dropped 4.5% this week to $1,024 per pound. This week’s national average wholesale flower price is off 8.2% from the recent peak of $1,115 per pound observed in late November.

The U.S. Spot wholesale flower price is firmly in a downtrend after the November double top formation. For the moment, wholesale prices remain up relative to a year ago, when the national average price dwelled under $1,000 per pound for essentially all of Q1 2023. Given price movement in major state markets, however, we may be headed back to the $950 – $1,000 range.

Wholesale flower prices in the large western markets of California, Colorado, and Oregon are all trending downward. Colorado’s spot price was the first to begin to decline after climbing through September and October last year. It was followed by Oregon’s in late November. The recent dive in California’s spot wholesale flower price follows a November – December runup, but can be seen as a continuation of the larger downtrend that began in June 2023.

The current price erosion in these markets indicates that talk of contracting cultivation that was commonplace last year may have been somewhat overblown. That was certainly the case in Oregon, where official data showed harvest volume to be essentially flat from 2022 to 2023.

In California, much has been made of declining cultivation license numbers, which are of course indisputable, but are an imperfect gauge of actual production. How much of the cultivation capacity of surrendered or lapsed licenses was actually producing remains unknown. The recent shuttering of Lowell Farms cultivation operations attests to the fact that declining license stats do include productive operations, but such losses are being offset by expanding production at larger scale operations such as Glass House.

In Colorado, data from the state shows that an actual production pullback did take place in 2023, yet price remains locked in the range that it entered in August 2022. It’s fair to say that even with a significant decrease in the number of plants being grown in 2023 that Colorado’s market is still oversupplied.

This is not necessarily surprising based on available data. The state Marijuana Enforcement Division last published production and purchase volume figures in its 2020 Annual Update, which was a year of record-breaking sales in Colorado with the arrival of the Covid-19 pandemic. Even in that year of elevated demand, licensed cultivators produced 40% more flower than was purchased by consumers and patients. Production expanded in 2021 and, even though it declined year-on-year in 2022, that year’s production in terms of plants grown was higher than in 2020. Now, as we’ve covered, sales are on the decline and in November 2023 fell to their lowest level since February 2017.

Overall, it will take much larger pullbacks in production to balance supply and demand in mature western markets in the current environment where interstate commerce remains illegal. Moving east, Michigan – the largest market east of the Mississippi River – is now also dealing with oversupply and low prices. As a younger market, production is still expanding and we have not yet reached the point where notable attrition is occurring amongst cultivators, though it is likely not too far off.

Ultimately, it would likely take a very large amount of production side businesses going under and exiting state-licensed markets in order to bring wholesale prices back up to levels seen in prior years. Such a prospect is surely unwelcome to the industry and to state officials; even federal lawmakers are unlikely to want thousands of lost jobs in their districts. To avoid such an outcome, however, federal reform beyond rescheduling is necessary.

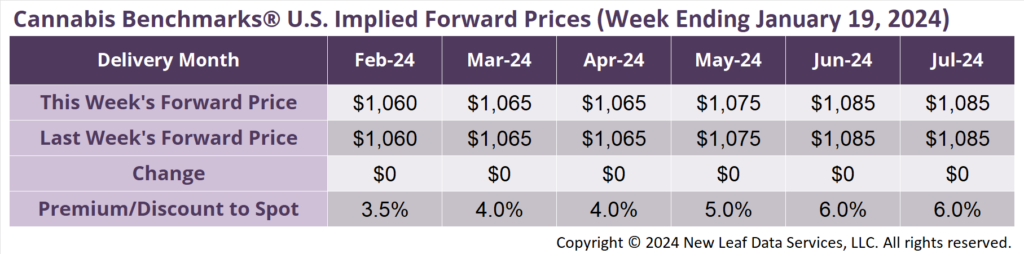

February 2024 Implied Forward unchanged at $1,060 per pound.

At $1,060 per pound, the February 2024 Implied Forward represents a premium of 3.5% relative to the current U.S. Spot Price of $1,024 per pound.

Wholesale Flower Prices Drifting Downward as State Tops $3 Billion in Sales in 2023

Social Equity Infusers Facing Anti-Competitive Market Structure, ‘Price Gouging’ – Interview

2023 Wholesale Price Downtrend Appears Over, New Direction Still Uncertain as Market Contracts

Report: Governor Proposes Repeal of Potency-Based Wholesale Tax