*The provincial excise taxes vary. Cannabis Benchmarks estimates the population weighted average excise tax for Canada.

**CCSI is inclusive of the estimated Federal & Provincial cannabis excise taxes..

The CCSI was assessed at C$5.09 per gram this week, down from last week’s C$5.14 per gram. This week’s price equates to US$1,807 per pound at the current exchange rate.

Include your weekly wholesale transactions in our price assessment by joining our Price Contributor Network

If you have not already done so, we invite you to join our Price Contributor Network, where market participants anonymously submit wholesale transactions to be included in our weekly price assessments. It takes two minutes to join and two minutes to submit each week, and comes with loads of extra data and market intelligence.

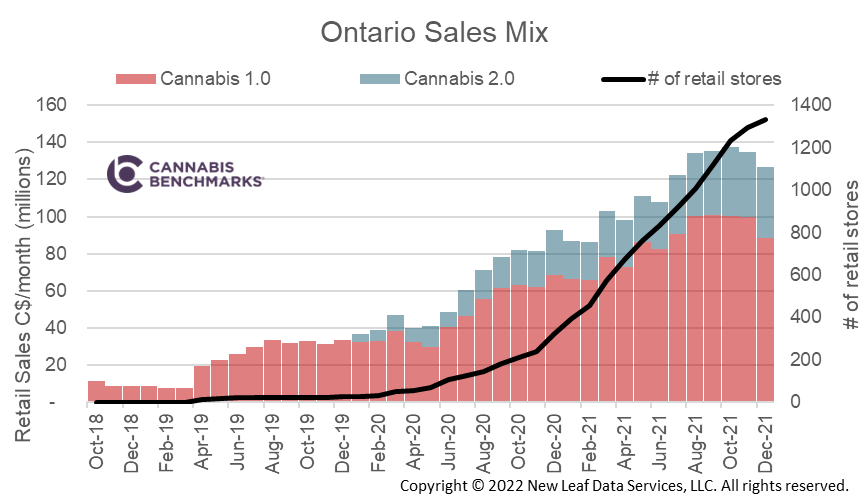

This week we continue to examine data published in the Ontario Cannabis Store’s (OCS) quarterly Cannabis Insights report, which covers the period from October through December 2021. The report contains a wide variety of useful data detailing how Ontario’s market has developed.

This report focuses on the proportion of sales dedicated to cannabis 1.0 and 2.0 products in Ontario. As a reminder, cannabis 1.0 refers to the legalization of combustible cannabis flower, cannabis oils, and cannabis seeds in October 2018. A year later cannabis 2.0 began, making available to consumers derivative products such as vapes, edibles, beverages, concentrates, and topicals. The data aggregated in today’s CCSI report reviews a series of OCS quarterly reports to compile a complete view of trends following the introduction of cannabis 2.0 products.

Cannabis 2.0 products created a lot of excitement ahead of their availability, and sales from the different product categories were expected to grow quickly. Now that we have over two years of data, we can see cannabis 2.0 products starting to make up a notable share of sales. As seen in the chart below, total cannabis sales in Ontario have been accelerating with the rapid build-out of brick-and-mortar stores. From December 2020 to December 2021, cannabis 2.0 product sales have jumped from making up 26% of total sales to over 30%.

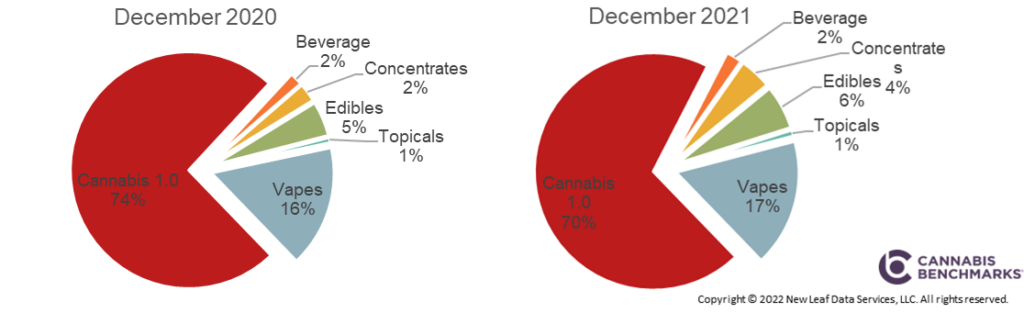

Diving deeper into the cannabis sales mix, we see that most consumers prefer the traditional smokeable or inhalable products (dry flower or vapes, respectively), with all other derivative products making up very small proportions of total sales. That said, modest increases in spending on edibles and concentrates can be seen in the chart below, which compares the sales mix from the end of 2020 and 2021.

The variety of cannabis 2.0 products is increasing and, as time passes, manufacturers are seeing which products are more popular amongst customers. The cannabis 2.0 products generally command a premium for the same cannabis input; hence we shall see more sales generated by this category as products become more accepted.