Image: Joel Muniz/Unsplash

Image: Joel Muniz/Unsplash

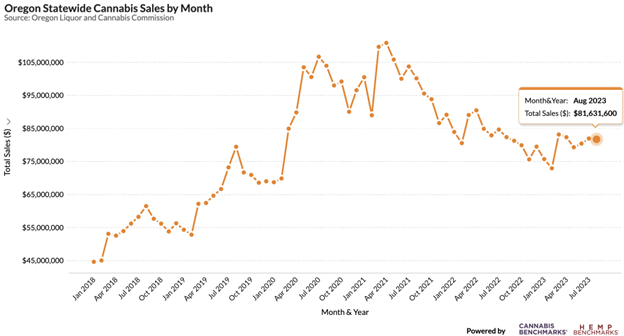

The Oregon Liquor and Cannabis Commission (OLCC) this week issued sales data for August 2023. August saw licensed retailers tally over $81.6 million in sales, down 0.5% from July sales of nearly $82.1 million and down 0.8% from sales of $82.3 million in August 2022.

Overall statewide sales are illustrated in the chart below. The steep downtrend that began after April 2021 and continued into early this year has flattened a bit under the spike that occurred in March. August’s nearly flat year-on-year sales movement is another indicator that demand is stabilizing.

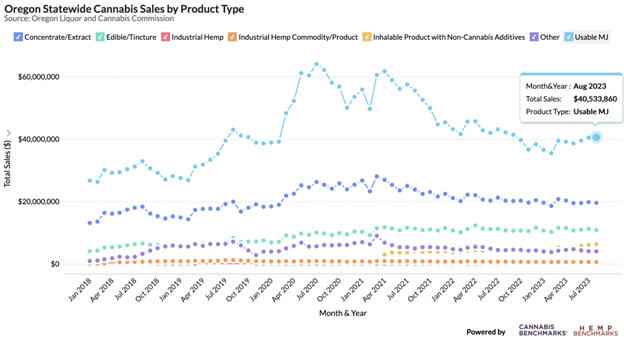

A breakdown of August sales by the major product types delineated by OLCC is as follows:

August 2023’s total harvest volume – encompassing indoor, outdoor, and mixed light licensees – was 667,267 pounds of wet weight, down 41.9% from August 2022’s total harvest of 1,148,924 pounds.

Monthly harvest figures for 2023 were down year-on-year in each month from February through June. July was the first month since January to see an increase in harvest volume compared to a year ago, and the first month to see a sizable increase.

We postulated last month that the jump in July 2023 harvest volume had more to do with weather conditions than growers increasing capacity. A particularly wet and chilly spring in 2022 resulted in growers getting plants in the ground later than usual, sources told us at the time, leading to relatively late summer and autumn harvests, including the large August 2022 harvest. It appears now that our speculation was correct given the significant year-on-year decrease in harvest volume seen in August 2023.

To better gauge how 2023’s summer crops stack up to 2022’s, we can compare the cumulative July-August harvest figures for each year. For July-August 2023, Oregon growers harvested a total of 1,240,712 pounds of wet weight, down 24.4% from 1,641,557 pounds of wet weight in July-August 2022. Overall it appears that the general decrease in production in Oregon observed in the first half of this year has continued into the summer, despite the month-to-month fluctuations resulting from varying weather conditions.

A breakdown of August harvest data by producer type is as follows:

For comparison, July 2023 saw a 24% year-on-year increase in mixed light harvest volume and outdoor harvest volume increased by a third compared to July 2022. As discussed just above, what looked like an expansion of production in July has ultimately turned out to be a sizable contraction in summer crops due almost exclusively to outdoor cultivators pulling back.

The median retail price for a gram of usable marijuana continued to climb in August. It has been on the rise since April, when the price often ticks downward month-on-month due to 4/20 discounts and promotions. The retail price of a gram of flower was $3.95 in August, up from $3.86 the month prior and from $3.69 in April 2023.

Median retail prices for concentrates and extracts remain relatively low at $16.00 per gram in August, flat from July and up from the all-time low of $15.75 per gram in April, but down from $16.67 per gram in August 2022.

Despite some volatility, Oregon’s overall spot wholesale flower price as of last week was off just 3.7% from a year. Last week’s wholesale price for indoor product was up 23.4% year-on-year. Greenhouse flower’s spot wholesale price declined 19.9% from the first week of September 2022 to last week. Meanwhile, outdoor flower’s spot wholesale price per pound in the opening week of September 2023 is essentially unchanged from from a year before, again despite volatility in the course of the previous 12 months.

As we reported in our Cannabis Benchmarks Premium Report last week, Oregon growers scored a win in court when a judge halted required testing for aspergillus that had commenced in March of this year. Cultivators and product manufacturers in the state had decried the tests, with many reporting failures and resorting to remediation or product destruction due to the presence of the environmentally ubiquitous fungi. With aspergillus screenings likely off the table for the remainder of the year and into 2024 at least, more supply should be able to come to market with lower costs to growers, putting downward pressure on wholesale prices as we head into the harvest season.